Before MEV, I Built a Rust AMM Lab to Measure Pool State

Part I asked whether a public-pool surface formed. This piece opens the pool and runs its state forward.

Part I compared canonical SPYx on Solana and Ethereum. Raydium and Orca showed substantial June volume; the one discovered Ethereum canonical pool returned 13 decoded swaps and $43.49 in USDC notional over June 1–21. Canonical deployment was present. Executable public-pool liquidity was not observed at the same scale.

That gap was measured from the outside: venue bars, swap counts, and route classes. It did not reconstruct reserves, fee accrual, arbitrage behavior, or what an LP would have held after external repricing.

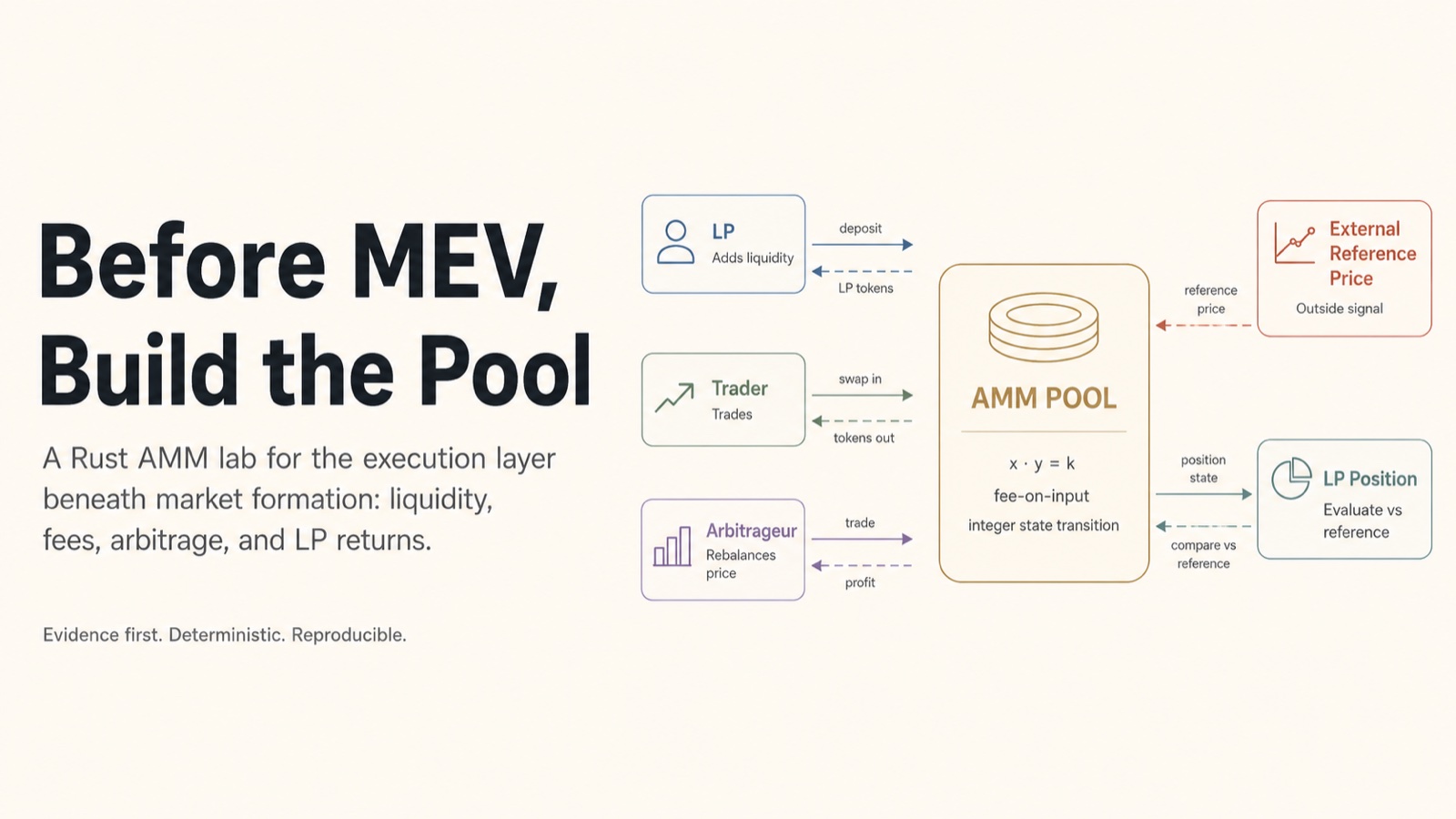

So I built a smaller Rust lab and stopped before MEV. The first question was not who could sandwich a trade. It was what the pool had to expose first: reserves, fee logic, slippage guards, arbitrage, and LP accounting.

How I run the lab

Each run is a TOML scenario: typed commands executed in sequence against u128 pool state. Fee-on-input, no floating point in reserves. Each command writes the next state; each scenario writes JSON and CSV to data/processed/.

Two blocks share the same CPMM rules. The deterministic block has four TOML scenarios, each a point event. The stochastic block has one seeded price path. Both write artifacts to data/processed/; claims map via research/evidence_ledger.csv (C1–C11).

cargo test --all

scripts/run_all_scenarios.sh

cargo run --release -- scenario run scenarios/<name>.toml

scripts/run_all_scenarios.sh runs all four deterministic scenarios. Scenario format: scenarios/README.md.

Fee-on-input ordering in src/swap.rs is what makes the measured cost separable from the curve:

let fee = amount_in * fee_bps as u128 / 10_000;

let amount_in_after_fee = amount_in - fee;

let amount_out = amount_in_after_fee * reserve_out

/ (reserve_in + amount_in_after_fee);

A slippage guard checks amount_out >= min_out before any state is committed.

I use four terms narrowly:

- Execution drag is the single-swap cost relative to the pre-trade pool spot: fee plus curve effect paid by the trader.

- LP-vs-hold is withdrawal value versus holding the original deposit through a deterministic shock.

- Tracking error / LVR is the path-level loss measure used in the Campbell-style run: the cost of passive liquidity while the external mark moves.

- Hedged PnL is fee revenue minus tracking error in the Campbell-style run.

Deterministic scenarios

Four files live in scenarios/. Same runner, same u128 pool. Each run fixes an input state, executes typed commands, and writes an artifact. Part I measured activity from the outside; these scenarios isolate pool-side mechanisms one at a time. They are not calibrated to SPYx.

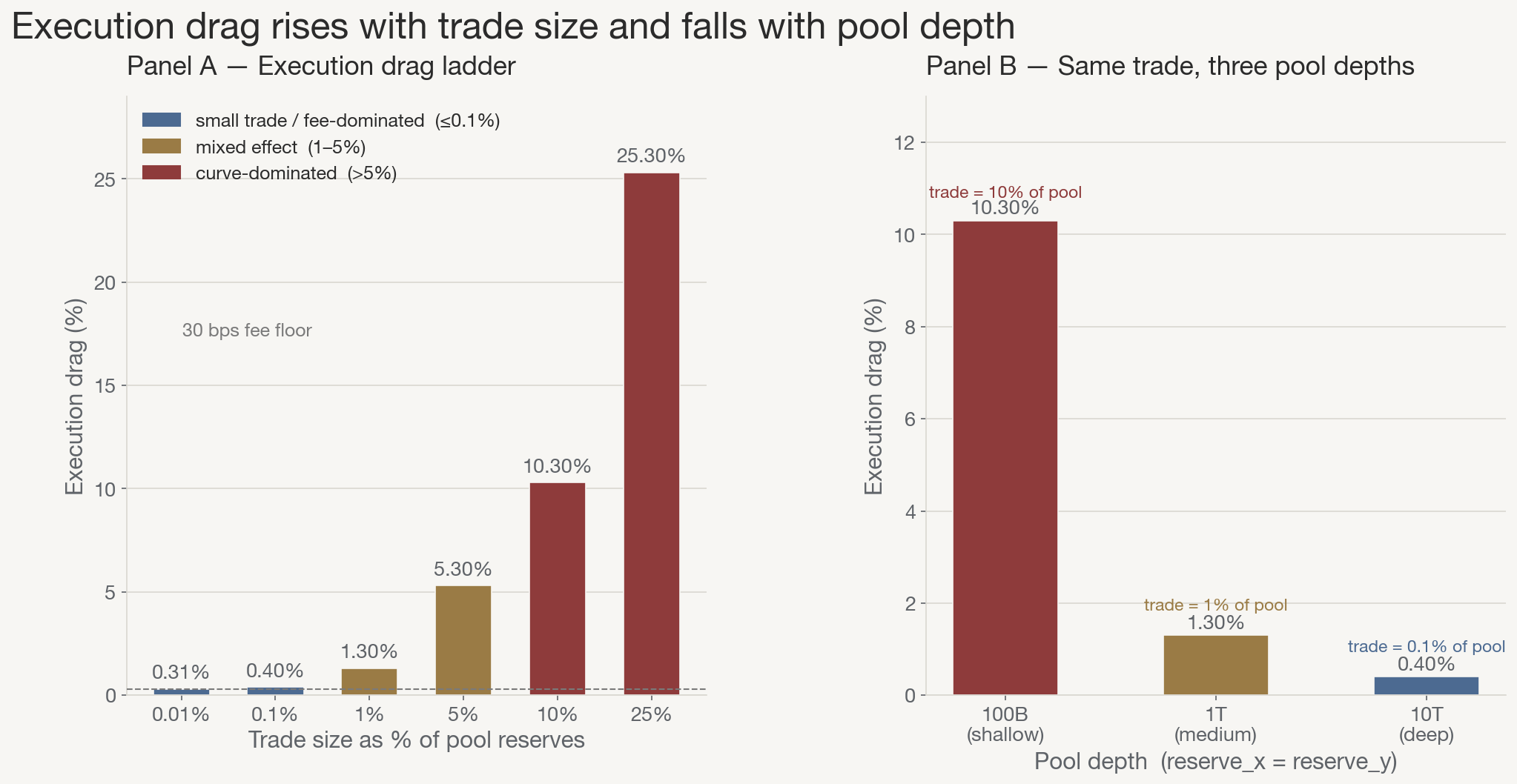

Trade size sets execution drag: price_impact_ladder.toml

-

Input. One 1T / 1T pool at spot 1.0. Six

SwapExactInruns from 100M to 250B base units (0.01% → 25% of reserves). -

Method.

SwapExactInwith 30 bps fee-on-input. I call the measured quantity execution drag: fee plus curve effect, not slippage.

execution_drag_pct = (execution price − pre-trade spot) / pre-trade spot

- Output.

price_impact_ladder_swaps.csv. Drag runs 0.31% at the smallest trade to 25.30% at 25% of pool, more than 80× the 30 bps fee floor (C1).

Same spot, different executable depth: same_price_different_depth.toml

-

Input. Three pools, all at spot 1.0: 100B, 1T, and 10T reserves. Same trade every time: 10B base units of X.

-

Method. Same

SwapExactIn. Only reserves change. -

Output.

same_price_different_depth_swaps.csv. Drag is 10.30% on the shallow pool, 1.30% on 1T, 0.40% on 10T (C2). Part I noted that nominal and executable liquidity diverge; this run holds the trade fixed and changes only reserves.

price_impact_ladder_swaps.csv, same_price_different_depth_swaps.csv.

External repricing leaves a fee-limited gap: arbitrage_repricing.toml

Part I treated arbitrage as correction against stale inventory, not theft from the pool. This run makes the correction explicit.

-

Input. 1T / 1T pool at 1.0.

ExternalPriceMovesets reference to 1.5. Pool price stays at 1.0 until someone trades. -

Method.

ArbitrageUntilNoProfituses ternary search on input size, because profit is unimodal. Too small and fees eat it; too large and the curve overshoots. -

Output.

arbitrage_repricing_arbitrage.csv. Pool reprices to 1.496, not 1.500. Residual gap: 0.00368. It is below the fee threshold, so no rational actor closes it (C3, C4). The oracle did not update the pool. A trade did.

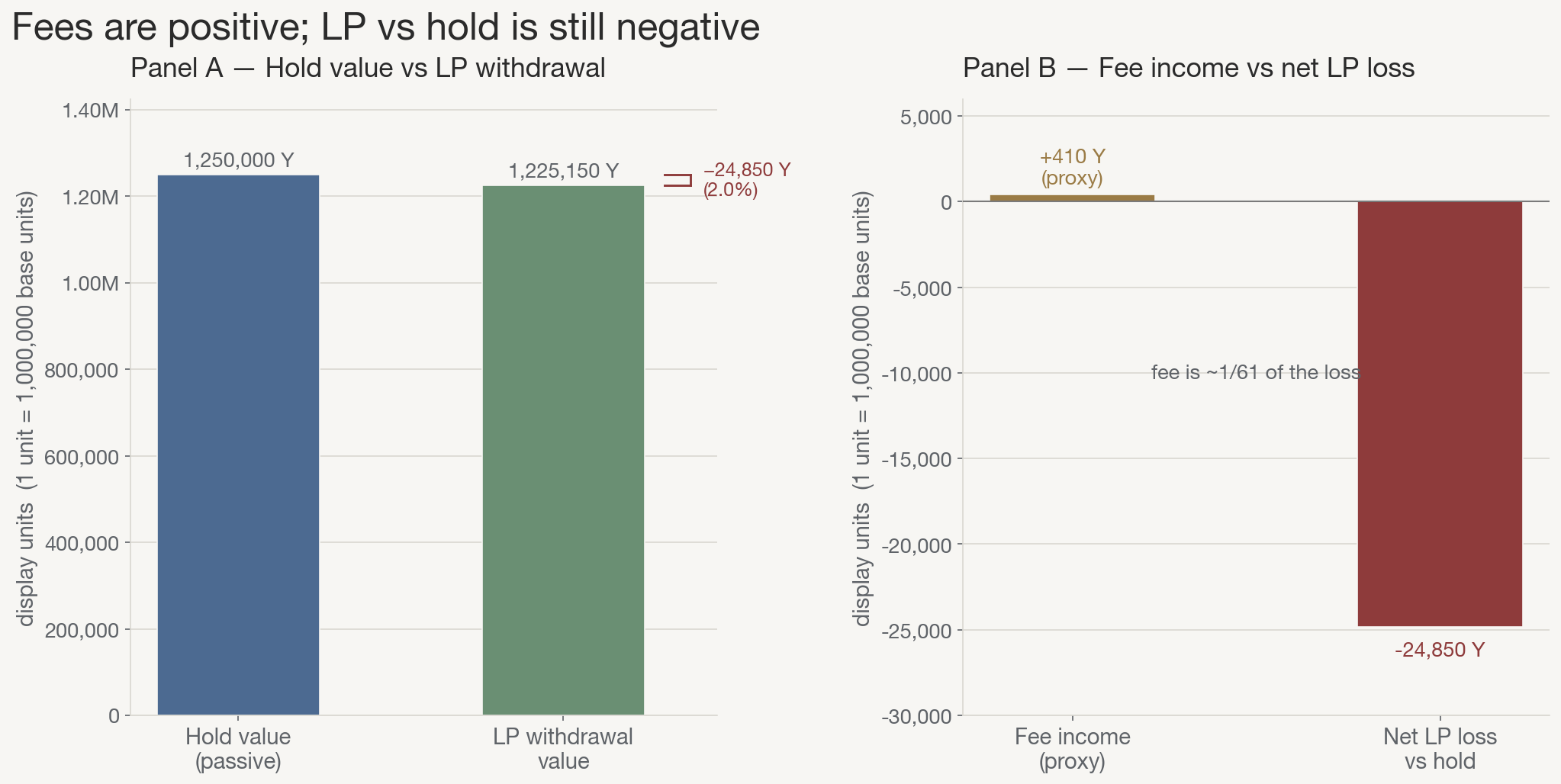

Fees accrued; hold still won: lp_vs_hold.toml

Part I asked whether fees compensate adverse selection when fundamental flow is thin. This run answers one controlled version. It is not 0xafdd…4575; it is a synthetic 1T / 1T pool under a 50% external move.

-

Input. LP deposits 500B X and 500B Y into a 1T / 1T pool. Three swaps run. External price moves to 1.5. Arbitrageur reprices once.

-

Method.

LpPerformancereports withdrawal value vs passive hold, with fee income separated. Display: 1 unit = 1,000,000 base units. -

Output.

lp_vs_hold.json. Hold 1,250,000 Y. LP withdrawal 1,225,150 Y. Fee income +410 Y. Net LP-vs-hold −24,850 Y. Fee income covered about 1/61 of the loss (C6, C7).

cargo run --release -- scenario run scenarios/lp_vs_hold.toml

lp_vs_hold.json.

Under this setting: fee income positive, LP-vs-hold negative. One shock, three swaps, one arb pass.

Stochastic scenarios

The deterministic block stops at point events. That is enough to see how size, depth, repricing, and a single LP shock behave. Part I’s passive-liquidity question is path-dependent.

Part I cited Campbell et al. (2025) on loss-versus-rebalancing: the cost of passively providing liquidity while the external mark moves. The paper’s object is not one 50% jump. It asks whether fee revenue accumulates faster than LVR when arbitrageurs and fundamental flow trade against the pool step by step. Part I could name that tradeoff; it could not run it.

lp_vs_hold.toml made the single-shock version concrete: fees +410 Y, net LP-vs-hold −24,850 Y. The stochastic block keeps the pool economics and changes the input: a seeded GBM price path, routed buy/sell demand each step, and cumulative fee vs tracking error over 1,440 steps. Implementation follows Campbell et al.’s reduced-form CEX + DEX model; the draw is fixed by seed = 42.

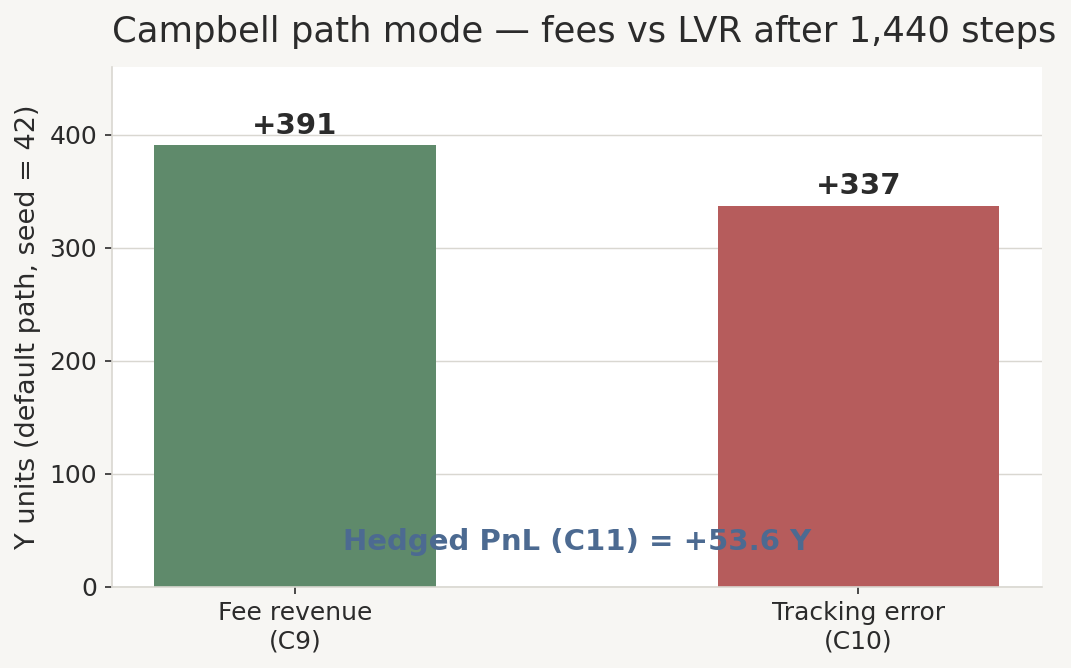

Fee revenue vs LVR over a path: campbell_sim.toml

-

Input. GBM CEX price (sigma = 0.04, seed = 42). 1M X / 500 Y reserves. 100 Y buy and sell demand per step. 1,440 steps.

-

Method. Separate binary (

src/bin/campbell_sim.rs).f64pool, three agents per step (arb → buy → sell). Not the TOML scenario runner.

cargo run --bin campbell_sim scenarios/campbell_sim.toml

# -> data/processed/campbell_sim.json

- Output. Fee revenue 390.78 Y (C9). Tracking error 337.16 Y (C10). Hedged PnL +53.62 Y (C11). Under this seeded path, fees outpaced LVR. The single-shock LP run had the opposite sign (C7). LP economics depend on path and flow intensity, not just whether fees are positive on one event.

campbell_sim.json.

Closing

The deterministic block made four pool-layer quantities visible: execution drag, depth, arbitrage residual, and LP-vs-hold. The stochastic block added one path-level quantity: whether fees accumulated faster than tracking error on a seeded Campbell-style run.

Those results are not a live-pool return model. They use synthetic reserves, one seeded path, and simplified flow. The next version should vary depth, fee tier, seeds, and flow assumptions before adding mempool ordering.

That is the boundary of this article: before modeling who captures a trade, the pool layer itself has to be specified and measured.

Appendix

- Repo: egpivo/amm-lab

- Deterministic:

price_impact_ladder.toml,same_price_different_depth.toml,arbitrage_repricing.toml,lp_vs_hold.toml - Stochastic:

campbell_sim.toml - Campbell: Campbell, J., Bergault, P., Milionis, J., and Nutz, M. (2025). Optimal Fees for Liquidity Provision in Automated Market Makers. arXiv:2508.08152.

- Evidence ledger:

research/evidence_ledger.csv(C1–C11) - Part I: The token appeared twice. The AMM market formed once.