The SpaceX Trade Exists. Now Watch the Tape.

SpaceX stock is not public yet, but SPCXUSDT perps already show volume, open interest, funding, and venue concentration. The question is what this tape can—and cannot—tell us.

This follows my previous post, Tokenization Is Not Just Putting Assets on a Blockchain: the broader claim was that tokenization is infrastructure, not a wrapper. SPCXUSDT is a concrete instance of that—access moved before the asset did.

Castle Labs is the trigger, not the thesis

Castle Labs recently framed this category as pre-IPO markets moving onchain (see post). That is the market conversation, not my argument. My question is narrower: what does the tape actually show, and what would change if this stopped being a quiet market?

Conjecture: tokenization moves access before ownership

Tokenization is usually described as moving assets or ownership onchain. In practice, the first layer to move may be access to a story: the ability to take a position on a private-company valuation before public equity exists.

SpaceX makes that concrete. All three crypto venues (Bitget, Binance, and Bybit) listed SPCXUSDT perpetual contracts on May 21, 2026, before any public SpaceX equity existed. Republic had already introduced rSPAX, a SpaceX-linked Mirror Token product, in late 2025.

This is not a claim that the products are wrong. It is a claim about sequencing: access moved first.

That changes what matters. If access arrives before ownership and before a full public risk tape, the useful question is not “is this onchain?” It is: what can the tape show, and what is still not externally observable?

The SpaceX trade is already measurable

At 03:31 UTC on 2026-05-26, public REST APIs returned the following without authentication.

| Venue | 24h volume | Open interest | Funding | Max leverage |

|---|---|---|---|---|

| Binance | $22.5M | $29.7M | ~0.005% | not confirmed (auth required) |

| Bybit | $878K | $1.3M | 0.0% | 10× |

| Bitget | $1.87M | $3.7M | 0.0% | 5× |

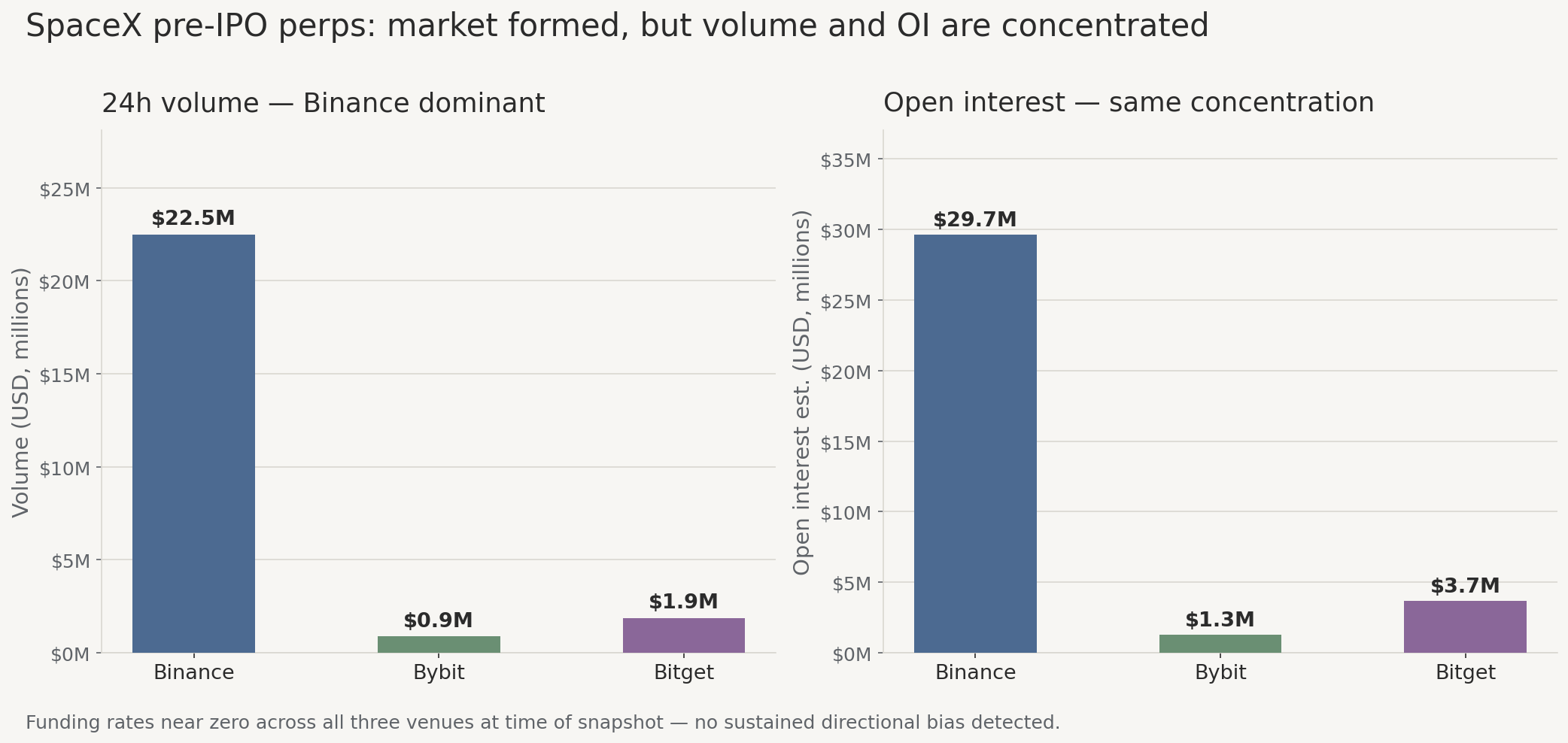

| Total | ~$25.2M | ~$34.6M | — | — |

This is not only a product page. At that snapshot, it was a measurable market.

Concentration is the first thing to read off the table: Binance accounts for ~89% of 24-hour volume and ~86% of open interest. That is not a three-venue market in equal weight. Any Binance-specific issue (operational, regulatory, or pricing-related) would matter disproportionately for the observable tape.

What the holder actually receives is also worth stating clearly. All three perps are USDT-settled synthetic derivatives. Trader margin supports the exchange derivatives product; it is not primary capital paid to SpaceX. No equity transfers. No ownership, voting, or dividend rights. The holder gets synthetic price exposure to an estimated SpaceX valuation, not a claim on SpaceX stock.

Republic describes rSPAX as a Mirror Token structured as a contingent payout note linked to SpaceX, not as direct equity. Its capital path is not clearly documented in the reviewed materials. It is context for the broader pre-IPO access category but not part of the API tape above; no public secondary market for rSPAX was found.

Interpretation: “Pre-IPO perp” is not one product. It is a shared label across venue-specific USDT-settled synthetics, each with its own leverage limits and insufficiently public index methodology. The shared label hides those differences.

What does not look stressed yet

The current snapshot has none of the signals typically associated with a stressed synthetic market.

Funding is near zero at all three venues. Bybit showed five consecutive 8-hour periods at 0.0%. Bitget showed 0.0%. Binance showed about 0.005%, close to zero and not obviously directional. No side is paying a sustained premium to hold the position.

Prices are tight: $208.04 on Binance, $208.42 on Bitget, $208.74 on Bybit, a spread of $0.70, roughly 33 basis points. That is consistent with cross-venue alignment. It does not tell you how each venue sources its pre-IPO reference value.

The latest Alternative.me reading used here was 30/100 (“Fear”) on 2026-05-25. That is not a broad risk-on backdrop. SPCXUSDT showing $25.2M in 24-hour volume in that context is at least consistent with a SpaceX-specific narrative trade.

Note: None of this is proof of stability. These signals can shift quickly if a listing window becomes concrete.

What I would watch next

The snapshot is quiet, but quiet is not the same as safe. I would watch five fields in the next pull: OI / volume, funding, venue concentration, price dispersion, and onchain spillover.

-

OI / volume. Current ratios are 1.32 (Binance), 1.46 (Bybit), 1.97 (Bitget). Not extreme. If OI rises while volume stays flat, leveraged inventory is building without matching activity.

-

Funding. Quiet now. The warning sign is persistent non-zero in either direction; one-sided accumulation shows up here before it shows up in price.

-

Venue concentration. Binance carries ~89% of volume and ~86% of OI. Any Binance-specific disruption (operational, regulatory, or pricing) would matter disproportionately. Watch for abrupt migration to or from Binance.

-

Price dispersion. Venues were aligned at ~33 bps in this snapshot. Widening dispersion near the reported listing window is more signal than headline price drift.

-

Onchain spillover. No SPCX-named contract, pool, wrapper, or vault found on Ethereum or Base. This is currently a CEX perp story. If that changes, the risk monitor expands: oracle dependency, AMM slippage, MEV exposure, and liquidation triggers on an estimated private-company valuation all become relevant.

In short: volume tells me the trade exists; OI tells me whether risk inventory is building; funding tells me whether positioning is one-sided; dispersion tells me whether venues remain aligned; onchain spillover tells me whether this becomes composable.

Closing

SpaceX equity does not trade publicly. A synthetic market around SpaceX already does, observable without an account, spread across three venues, with real volume and open interest. The sequencing is the finding: access moved first. The tape is visible. The index methodology, position concentration, and liquidation mechanics are not.

Hypothesis I would monitor: the tape may stop being quiet as the reported listing window approaches. The first useful signal may come from funding, OI, or cross-venue dispersion rather than headline price alone. It could be funding turning persistently non-zero on Binance, or a venue price stepping away from the other two without an announced index change. That is when “pre-IPO perp” stops being a label and starts being a position-concentration problem.

Where I would spend the next snapshot: rolling funding across all three venues, OI / volume ratio drift, cross-venue price dispersion, and any first appearance of an SPCX-named contract on Ethereum, Base, or Arbitrum. The index methodology question is the one I would ask each venue directly, not infer from prices.

Appendix: data sources and reproduction

Snapshot: 2026-05-26 ~03:31 UTC. Public REST APIs, no authentication:

- Binance USDⓈ-M Futures API (

premiumIndex,openInterest,ticker/24hr) - Bybit V5 API (

tickers,funding-history,instruments-info) - Bitget API v2 (

tickers,contracts)

Derived columns.

- OI in USD = base-contract OI × last price.

- OI / volume ratio = open interest ÷ 24h volume.

- Price dispersion (bps) = (max − min) / mid × 10,000.

Leverage and funding.

- Bybit 10× and Bitget 5× max leverage confirmed from public

instruments-infoandcontractsendpoints. - Binance

leverageBracketrequires authentication; not confirmed here. - Bybit

funding-historyreturned 5 consecutive 8-hour periods, all 0.0%. - Bitget current funding 0.0%.

- Binance

premiumIndexlastFundingRate ~0.005%.

Onchain check.

- Alchemy RPC on Ethereum (blocks ~25142281–25175909) and Base (blocks ~46280529–46483011) over 2026-05-21 → 2026-05-26.

- No SPCX-named contract identified. Stablecoin transfer volumes sampled but not attributable to SpaceX without product contract linkage.

Regime context. Crypto Fear & Greed Index from Alternative.me, 2026-05-25: 30/100 (“Fear”).

Scope. “Not publicly documented” means not found in public-facing venue documentation reviewed as of 2026-05-26. This post does not assess reserve adequacy at any venue, regulatory compliance of the products, or the fair value of an SPCX position.

References: